What is the CSRD?

The Corporate Sustainability Reporting Directive (CSRD) is a regulation introduced by the European Union (EU) to enhance and standardise sustainability reporting across companies. It aims to improve the availability and reliability of sustainability information, promoting transparency around companies’ impacts on people and the environment.

The CSRD replaces the existing Non-Financial Reporting Directive (NFRD) and introduces more comprehensive reporting requirements.

Who does the CSRD affect?…Compliance does roll downhill!

Just because you are maybe a SMB, or smaller than the initial criteria, it doesn’t mean it won’t affect you…at some point.

With the growing focus on Scope 3 emissions and the necessity for supply chains to align with company commitments, the end customer will mandate that clients furnish the reporting data essential for their compliance.

Source: Normative: Decoding CSRD: Handbook for the Corporate Sustainability Reporting Directive

The CSRD affects a wide range of companies, including:

- Large EU public interest entities with transferable securities traded on an EU-regulated market and with more than 500 employees.

- Large EU undertakings and EU parent undertakings of large groups.

- Non-EU companies with significant activity in the EU, including those listed on an EU-regulated market.

- Listed SME’s (Small and Medium-sized Enterprises) on EU-regulated markets, although they will have proportionate standards

What about UK companies? I’m based in the UK so why should it matter?!

UK companies, especially those with significant operations or listings in the EU. Here are some key points:

1. Scope: The CSRD applies to UK companies if they have securities listed on EU regulated markets or if they generate more than EUR 150 million net turnover in the EU for each of the last two consecutive financial years and have at least one EU subsidiary or branch

2. Reporting Requirements: Companies will need to report on various sustainability-related aspects, including their business model and strategy, sustainability targets, governance, policies, due diligence processes, and principal sustainability risks. Synnovate

3. Preparation: UK companies with European parent companies might be asked to report more non-financial data within their group structure.

Confused of the type of report and compliance required for CSRD or other up and coming regulation? Have a chat with Synnovate and we can help.

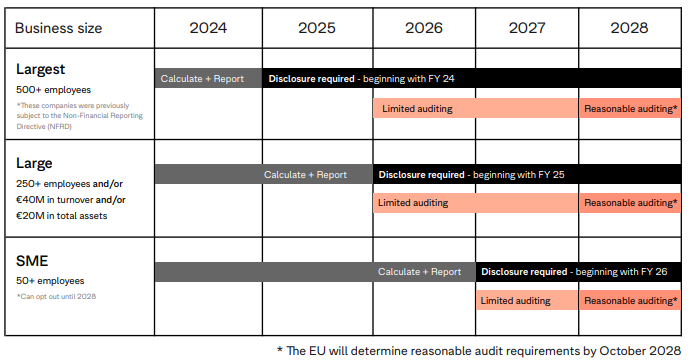

When Do I need to be compliant?!

How do you need to be compliant with the CSRD?

To be compliant with the CSRD, companies need to:

1. Determine if they are in scope: Companies must assess whether they meet the criteria for CSRD applicability, such as having significant activity in the EU or meeting specific size thresholds (e.g., net turnover of more than €40 million, balance sheet assets greater than €20 million, or more than 250 employees)

2.Prepare sustainability reports: Companies must produce disclosures in accordance with the European Sustainability Reporting Standards (ESRS), covering a broad range of sustainability topics using a “double materiality” approach. If you have already created an SECR report, you will be able to utilise the same information. Synnovate suggests adopting a Carbon Accounting platform to assist the company and its users in gathering data, monitoring relevant metrics, and reporting on that data. There are multiple platforms out there, some with mixed levels of performance. As much as Synnovate is vendor diagnostic, we have found the paid version of Normative to be quite useful for some of our customers care significantly about their Scope 3, and also the accuracy of the data breakdown.

3. Ensure data accuracy: Reported sustainability information must be assured to ensure its reliability and accuracy. The important of accuracy is going to increase over the next few years, and in particular Scope 3 should become easier as more companies adopt.

4. Adopt a risk-based approach: Companies should prioritise impacts based on severity and likelihood, focusing their due diligence efforts on areas of heightened risk.

What are the risks of non-compliance with the CSRD?

To date, there haven’t been many instances of fines, but as regulations increase, this may change. Compliance remains a critical element for the FinTech and MedTech sectors Synnovate serves, and the GreenTech sector has distinct reputation requirements to uphold.

Legal consequences: Corporations might be subjected to administrative disciplinary actions, which could include public disclosure of the infraction, mandates to alter practices, and monetary penalties.

Economic impacts: Failing to comply may lead to monetary fines and other economic penalties².

Reputation effects: A company’s image can be negatively affected, resulting in decreased confidence from investors and limitations in the market.

Operational disruptions: Compliance issues can cause operational complications and impede the development and upkeep of partnerships.

Loss of potential growth: Organisations risk losing potential avenues for expansion and attracting investments if they do not adhere to regulations. Synnovate has recognised an increased relevance of sustainability considerations in RFPs.

Normative Platform and CSRD – How can they help?

Normative can assist with CSRD compliance by providing a comprehensive carbon accounting platform that automates data collection, calculations, and reporting. This platform enhances auditability and supports regulatory compliance by ensuring data accuracy and transparency, which is crucial for audit purposes and compliance with CSRD requirements

I hope this FAQ helps you understand the key aspects of the CSRD and how Synnovate and Normative can assist with compliance! If you have any more questions, feel free to ask.